NBFC Refers to Non-Banking Financial Companies. As the name suggests they are not banks but are referred to as Shadow Banks. If we go by the definition of the RBI (RESERVE BANK OF INDIA) ACT, a Non-Banking Company carrying on the business of a Financial institution will be an NBFC. It Further States that the NBFC must be engaged in the business of Loans and Advances, Acquisition of stocks, equities, debt, etc issued by the government or any local authority.

But if Banks exist already then what is the need for NBFCs? In this article, we will go into detail about what NBFCs are, what they do, what the types of NBFCs and the difference between banks and NBFC.

Table of Contents

ToggleWhat are NBFCs(Non Banking Financial Companies)?

Any Non-Banking Company that works as a Financial Company can be categorized under NBFC. There are more than 8 Million MSMEs(Micro, Small & Medium Enterprises) in India. They are basically people or groups of people who run small businesses. For Example a Vegetable Shop, Individual Barbershop, or any small business shop owner.

Now it is a bit difficult for them to get a Loan from a Bank and even if they get it will be at a very high interest rate. Banks are very mindful of their NPA(Non-performing Assets) ratio and they don’t want it to go upwards. Providing Loans to MSMEs is risky for Banks as small business owners may not be able to repay the loan along with interest timely due to improper or irregular cash flows(earnings).

So, NBFCs help these small businesses even individual households with their financial needs.

What are Business of NBFCs?

- Lending: NBFCs can Issue Loans.

- They can Acquire/Invest in Shares, Stocks, Bonds, and Debentures issued by Government or other authorities/companies.

- Insurance: NBFCs can sell Insurance Policies.

- They can also accept deposits(Time Deposite/Fixed Deposite) but not Demand Deposits.

Difference Between Banks and NBFCs

NBFCs(Non-Banking Financial Companies) can Lend Money and Invest in various Stocks, Shares & Debentures just like Banks but there are a few differences as below:

- NBFCs cannot accept Demand Deposit, however, they can accept timed deposits like FD. Demand deposits are normal deposits in a bank where you can withdraw money whenever you need it without informing the bank via Cheque, ATM, or Digitally(Net Banking, UPI, etc).

- NBFCs can’t Issue Cheques or do not provide any payment or settlement system.

- No Insurance or Credit Guarantee on Fixed deposits in NBFCs, unlike Banks. If a particular NBFC is declared bankrupt then the deposited amount can’t be recovered.

NBFC vs Banks

| Features | Banks | NBFCs |

|---|---|---|

|

LENDING |

|

|

|

INVESTMENT |

|

|

|

INSURANCE |

|

|

|

PAYMENT SERVICES |

|

|

|

TIME DEPOSIT |

|

|

|

DEMAND DEPOSIT |

|

|

|

CHEQUE

DEPOSIT/WITHDRAW |

|

|

|

GURANTEE ON DEPOSIT |

|

|

Restrictions on NBFCs

RBI(Reserve Bank of India) regulates both Banks and NBFCs. However, the Regulations for banks are more strict as compared to NBFCs and that is why NBFCs are restricted in business that are associated with High Risk and can be Volatile. These include:

- Industrial Activities

- Agricultural Operations

- Sale and Purchase of Immovable property and services related to it.

Actually, NBFCs can operate in these businesses but it should not be their primary or principal business. It means the total revenue from any of these businesses should not exceed 50% of their total operational revenue.

List of Top 10 Upper Layer NBFCs in India

| Company | CoR for Public Deposit | Category | Layer |

|---|---|---|---|

|

Aditya Birla Finance Limited |

NO |

ICC |

UPPER |

|

Bajaj Finance Ltd. |

YES |

ICC |

UPPER |

|

Cholamandalam Investment and Finance Company Limited |

NO |

ICC |

UPPER |

|

HDB Financial Services Limited |

NO |

ICC |

UPPER |

|

L&T Finance Limited |

NO |

CIC |

UPPER |

|

Mahindra & Mahindra Financial Services Ltd |

YES |

ICC |

UPPER |

|

Muthoot Finance Limited |

NO |

ICC |

UPPER |

|

Shriram Finance Limited |

YES |

ICC |

UPPER |

|

Tata Capital Financial Services Limited* |

NO |

ICC |

UPPER |

|

Tata Sons Private Limited |

NO |

CIC |

UPPER |

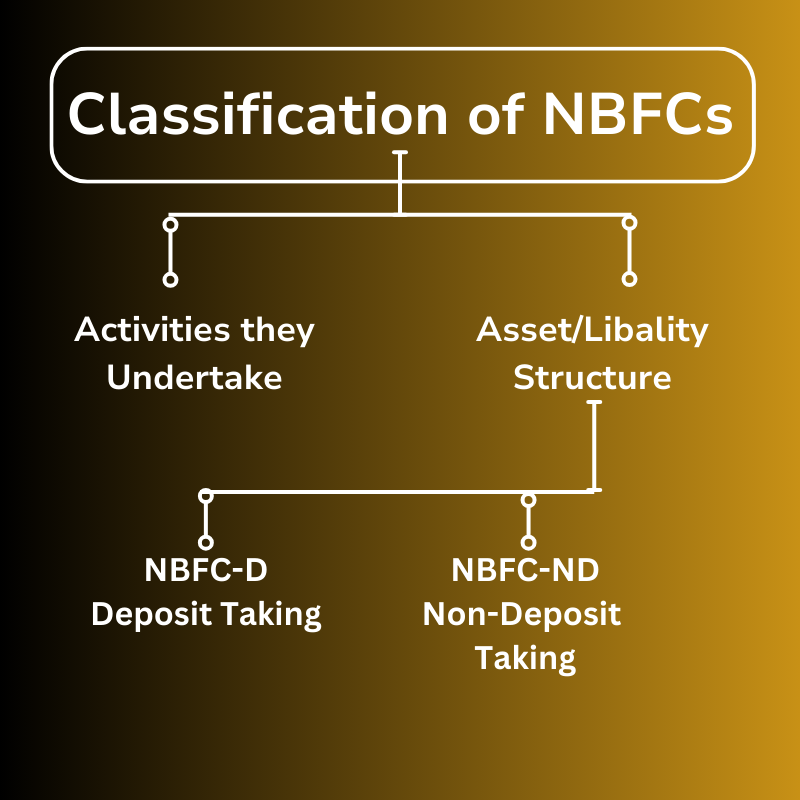

Different Types of NBFCs(Non-Banking Financial Companies)

NBFCs(Non-Banking Financial Companies) can be broadly classified under 2 categories based on ACTIVITIES THEY UNDERTAKE and ASSET/LIABILITY STRUCTURE.

NBFCs Type based on Asset/Libality Structure

Based on Asset/Liability Structure NBFCs can be divided into 2 parts. NBFC-D and NBFC-ND. NBFC-D means deposit taking NBFCs and NBFC-ND means Non-Deposit taking NBFCs.

The General Public can’t deposit money in NBFC-ND. Then what is the source of their fund and how will they do credit lending? Non-deposit NBFCs source their funding from markets and banks.

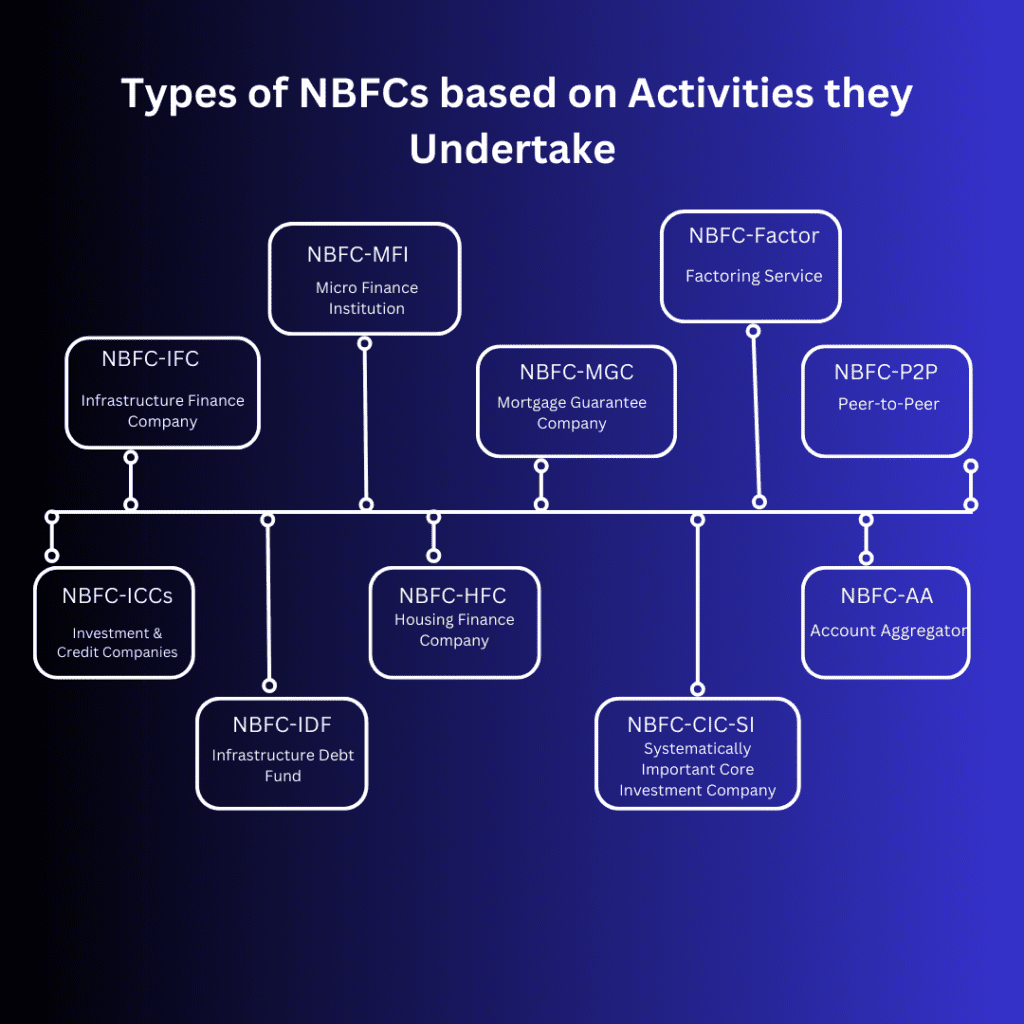

Types of NBFCs Based on Activity they Undertake

Based on which kind of activity NBFCs are involved in, they can be classified into 10 types.

- ICCs(Investment & Credit Companies): They offer a wide range of Financial products and services including loans, leasing, hire purchase, and other credit facilities. A few popular NBFC-ICCs in India are Aditya Birla Finance Limited, Bajaj Finance Ltd., L&T Finance Limited, Muthoot Finance Limited, etc.

- IFC(Infrastructure Finance Company): These companies are involved in facilitating loans for long-term infrastructure and real-estate development projects. A few popular companies under this category are India Infrastructure Finance Company Limited, Aseem Infrastructure Finance Limited, Indian Railway Finance Corporation Ltd, etc.

- IDF(Infrastructure Debt Fund): These companies are also involved in funding Infrastructure Projects but not by directly providing funding. They invest in debt securities of infrastructure companies and do not provide direct Loans. A few popular Companies under this category are India Infradebt Limited and NIIF Infrastructure Finance Limited.

- MFI(Micro Finance Institution): They Provide small amounts of loans to low-income individuals in rural and semi-urban areas for farming, small businesses, and self-employment. A few companies under this category are Sonata Finance Private Limited, Spandana Sphoorty Financial Ltd., and Annapurna Finance Private Limited. etc.

- HFC(Housing Finance Company): These companies are involved in facilitating loans to Individuals and Businesses for the purchase, construction, and renovation of residential properties.

- MGC(Mortgage Guarantee Company): They provide mortgage guarantee services to lending institutions such as banks, housing finance companies, and other NBFCs.

- CIC-SI(Systematically Important Core Investment Companies): These companies are involved in providing long-term Investment in core sectors of the economy such as infrastructure, manufacturing, and services.

- Factor: They provide Factoring Services to businesses, which can improve their cash flow and working capital management.

- P2P(Peer to Peer): These companies neither accept deposits nor provide loans. They provide a platform for individuals and businesses to borrow and lend money directly to each other through an electronic platform. These companies benefit from commissions on transactions through their electronic platform.

- AA(Account Aggregator): They provide a platform that allows individuals to view their financial information from multiple sources in one place like a Dashboard. For example, suppose you have a few FDs in HDFC Bank, Mutual Funds in ICICI Direct, Stocks investment in Zerodha, and Home loan from Kotak Mahindra. An Aggregator will aggregate and show you all the info in one place and you don’t need to visit all different platforms.

What is Factoring Service?

Factoring is a Financial Transaction in which a company sells its outstanding invoices/bills to a third party at a discount in exchange for immediate cash to maintain cash flow working capital.

Suppose Company A sells a few Products or Services to Company B. Company A will issue a bill/invoice and Company B will pay for it. But payment of bills does take time in businesses they are not settled immediately.

In this situation, there might be a Cash Crunch at Company A’s end to maintain their operations. In this case, Company A can avail services of NBFC-Factor companies. Company A can claim the cash part based on the bills from Factor Company and after that, it is the responsibility of Factor Company to take the bills from Company B.

Factoring Companies do charge a certain amount from Company A that can be accommodated in the bill amount as a discount.

What is need of NBFCs if Banks already Exists?

NBFCs are needed to cater to the financial needs of MSMEs(Micro, Small & Medium enterprises) in India. The Financial Needs of a small Vegetable Shop or Pan Shop Owner may be quite different from that of a big business and Banks may not agree to sanction loans to them due to their irregular cash flows and uncertainty in business.

What are systemically important NBFCs?

NBFCs whose asset size is ₹ 500 cr or more as per the last audited balance sheet are considered systemically important NBFCs. The reason for such classification is that the activities of such NBFCs will have a bearing on the financial stability of the overall economy.

How NBFCs are Different from Banks?

NBFCs are also involved in Financial business like Banks but the Rules & Regulations for NBFCs are not as strict as Banks and norms for NBFCs are less stringent.

- NBFCs can’t provide the facility of Demand Deposit.

- NBFCs can’t Issue Cheques.

- RBI does not Provide any guarantee on money deposited via Timed Deposit in NBFCs.